Used car ecommerce in GCC

We are in early stages of digital transformation of the world. Like other industries, used cars sales are not immune to this trend.

On the surface used cars seem to be ideal replacement for offline experience. Visiting a used car dealership is an unpleasant experience and even the nomenclature “used car salesman” has negative connotations.

In USA the used car industry has been disrupted by Carvana[1] , which can be considered an apex predator of the space[2]. In Europe, Auto1 group[3] is trying to position itself as the Carvana of Europe. We have seen many similar players emerging in the GCC region. Before delving into the used car ecommerce in GCC, lets take a detour to look in the key economics of the business and look deeply into the secret sauce of Carvana .

Overall, ecommerce is a mediocre business. The thought may surprise most people who always think of Amazon as a success story. In ecommerce you may have 1P business where you buy and hold your inventory and 3P business where you connect buyers and sellers as a marketplace. Amazon does both and derives more value from its 3P business. 1P requires substantial scale and Amazon just invested US$ 60 billion to build the scale in 2020 even at its current scale.

Used car ecommerce is even more challenging especially in 1P model. You need to buy the inventory which has substantial cost, then recondition it and, since it’s a big ticket item, you may need to help with financing too.

The model works if you are vertically integrated AND have a big TAM (“Total addressable market”).

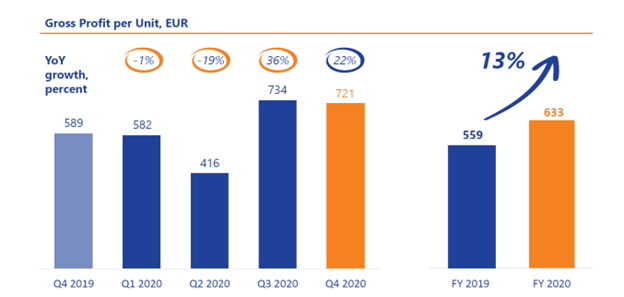

Here is a brief look at Carvana’s current financials and its long-term targets:

Carvana sold 425,237 units in 2021 and reached breakeven on EBITDA margin in 2021. The key matrix for a used car ecommerce place is Gross Margin Per Unit (“GPU”). What are the drivers of GPU?

In essence, buying from consumer or retail is cheaper than buying from wholesale or business customer. Converse is true, selling to retail is better in terms of pricing than to a wholesale customer. Hence the mix of inventory and selling channels are important. If we look at Carvana’s overall GPU it is now around US$4,500-5,000 whereas wholesale GPU is only around US$ 600. This reinforces the powerful impact that inventory mix and target customers can have on the margins.

But inventory and customer mix are one part of the overall picture.

As a vertically integrated used car ecommerce player there are many activities which need to be performed: you need to buy cars, fix, and transport them, sell and provide warranty etc.

But the killer value proposition of Carvana is something else. Carvana is a hidden auto loan bank too!

Carvana sells auto loans to customers, and it can INCREASE/DECREASE interest rates on those loans to compensate for the increase/decrease in the price of the cars.

Selling to retail customers is a big driver but the biggest driver of GPU almost 50% is “other gross profit” but what is this other gross profit?

Here is the definition as per the annual report of Carvana:

Other sales and revenues consist of 100% gross margin products for which gross profit equals revenue. Therefore, changes in other gross profit and the associated drivers are identical to changes in other sales and revenues and the associated drivers

In plain English, the other gross profit is basically gain on the sale of receivable to customers.

In effect the main driver of Carvana’s profitability is not straightforward ecommerce but the origination and sales of auto loans! It is in effect an auto loan financial institution masquerading as an ecommerce player.

There are other competitive advantages which Carvana enjoys. Carvana benefited from easy access to capital which enabled it to build the physical infrastructure.

USA is a continent size country, where building recondition centers and centralization inventory has acted as a moat for Carvana.

Now compare Carvana to German Auto1, which is positioning itself as a European Carvana. It sells much more cars than Carvana.

But the GPU is much lower.

The reasons are twofold: more retail business and lack of financing option.

In contrast to Carvana, Auto1 still mostly buys from consumers and sells to businesses (C2B).

Carvana is mostly a B2C business whereas Auto1 is exactly the opposite, i.e., buying retail and selling wholesale (C2B) hence the lower margin.

Initially I was skeptical whether a used car e-commerce player can successfully replicate the Carvana model in the GCC. But before delving further into the detail let’s take a survey of GCC used car (particularly UAE) ecommerce landscape.

There are three broad models:

1. Traditional players moving from offline to online: An example would be Al-Futtaim motors who have transitioned quite successfully to an omni channel model. Their online value proposition is very similar to Carvana.

2. Online auction houses: These are purely marketplaces for models and connect dealers with buyers. The main proposition is C2B. An example would sellanycar.com

3. The Carvana model: The main players are Kwak and Carzaty.

My skepticism about used car ecommerce in GCC stemmed from what I imagined would be a small TAM and lack of integrated options especially receivables securitization.

1. ME in general and UAE are geographically concentrated which precludes the need to develop a comprehensive infrastructure like Carvana and hence to build a physical moat around the business

2. Financing product is not available

3. The TAM is much smaller than USA and Europe,

4. There is another issue with different registrations and licensing stuff (Auto1 is still facing this issue)

But there are some peculiarities of the region which have enabled players like Carzaty to successfully emulate Carvana:

1. The car prices in Middle East are higher than the world. Because of cheaper oil and no taxation people have higher priced cars leading to an increased GPU per car

2. GCC is dominated by expatriates and people move in and out a lot hence the turnover is higher than other regions of the world

3. Financing is not needed because banks are very active in financing and lot of people have higher disposable income than the world average

The main moat of the players is not physical infrastructure like that of Carvana. The main moat is data which has been gathered by players over multiple iterations.

My gut feeling is there is a place for a pan GCC player who can consolidate across the region, but the issue remains the same, different countries different regimes. It is a very challenging business and jury is still out how much it can be scaled.

[1] https://investors.carvana.com/

[2] The current travails of Carvana are topics of discussions for another occasion